INVESTMENT PLANNING

Investment planning begins when you have a clear vision of your financial goals and objectives. Whether you are planning for retirement, your child’s education, or re-balancing your investments, having an investment strategy in place can take the stress out of your mind. With our team of tax and investment consultants, we can create an investment plan based on your goals, comfort with risk, and time horizon.

Registered Retirement Savings Plans

RRSPs give individuals the incentive to save towards their retirement. This incentive comes in the form of tax deductions. Any contributions that are made to an RRSP are deductible from your income for tax purposes, so they have the effect of reducing tax for the year.

RRSP’s are ideal for:

- individuals who don’t belong to a pension plan,

- individuals whose pension plans are inadequate

- individuals who want a higher retirement income than their pensions can provide

Advantages of RRSPs

- Tax savings and/or tax refunds

- Use up to $25,000 of your funds towards your first home

- Use a portion of your funds to pay for school (Lifelong Learning Plan – LLP)

- Tax sheltered growth

Advantages of TFSAs

- Tax-free growth on your investments

- No age limit for the TFSA – can contribute throughout retirement

- Withdrawn amounts can be contributed back the following year

- TFSA withdrawals are not considered as part of your income

Tax Free Savings Accounts

A tax-free savings account (TFSA) provides Canadians a way to earn investment income without having to pay tax. Individuals, 18 or older and who have a valid social insurance number can hold a TFSA.

Income earned in a TSFA or withdrawals will not affect eligibility for Old Age Security, the Guaranteed Income Supplement, the Canada Child Tax Benefit, the GST/HST Credit, or Age Credit. This makes the plans especially attractive for individuals whose taxable investment income would reduce benefits from these programs.

Registered Education Savings Plans

Many parents see education as the launching pad to a better career and a better life . But it comes at a cost . The University of Toronto has estimated the costs of one year at university at $27,050 . Here’s a summary of their calculation:

| Tuition* and fees | $7,550 |

| Residence fees, including a meal plan | $15,700 |

| Books and supplies | $1,000 |

| Personal expenses | $1, 000 |

| Spending money (varies per student) | $2 , 500 |

| Total | $27,750 |

*Costs will vary depending on the program of study . (Source: University of Toronto’s A Guide for Parents: Student Financial Planning and Support 2015-2016)

And the costs are going up . Over the last decade, university costs have been outpacing inflation . Here is an estimate of the future cost of education for a child born in 2016, using a 3% inflation rate:

| University costs for one year (see above) | $27,750 |

| Multiplied by 4 years | $111,000 |

| Assumed annual inflation of 3% over 18 years | $188,970 |

According to Statistics Canada, the post-secondary education inflation rate has tripled between 1990 and 2016 . Erring on the conservative side and using an inflation figure of 5% and 7% for tuition costs only in the above example, the future cost of education becomes $267,135 and $375,172 respectively!

GOVERNMENT GRANTS & BONDS

The Government of Canada provides further incentive to individuals saving for their children’s education through the Canada Education Savings Grant (CESG). The government will make a matching grant of 20% of the first $2,500 contributed each year to the RESP. For families with net incomes between $47,630 and $95,259, the additional grant is 10% on the first $500 of contributions.

If you contribute $2,500, the amount of CESG you will receive is set out below:

| FAMILY NET INCOME (2018) | ADDITIONAL CESG | BASIC CESG | TOTAL GRANTS |

| Less than $46,605 | First $500 x 20% = $100 | $2,500 x 20% = $500 | $600 |

| $46,605 – $93,208 | First $500 x 10% = $50 | $2,500 x 20% = $500 | $550 |

| More than $93,208 | First $500 x 0% = $0 | $2,500 x 20% = $500 | $500 |

For more detailed information regarding RESPs, Grants & Bonds, please visit the Government of Canada website.

RESP BASICS

- No annual contribution limit but there is a lifetime maximum of $50,000 for each beneficiary

- Contributions can be made over a 31 year period, and the RESP must be matured and fully paid out within 35 years

- The principal contributions are not tax-deductible and can be withdrawn tax-free any time

- Any growth remains tax-sheltered until it is paid out as educational assistance payments to the beneficiary

- Lower income families receive an additional grant of 10%

- Any unused CESG can be carried forward for use in another year, to a maximum of $1,000 per year

- Maximum lifetime grant per beneficiary is $7,200

WHAT IF MY CHILD DOES NOT PURSUE POST-SECONDARY EDUCATION?

- Wait a while – Your child may change his or her mind about going to school. RESP accounts can remain open for 36 years.

- Choose a new beneficiary – You can name an alternate beneficiary to receive the RESP income. In a family plan, the new beneficiary must be related by blood or adoption to the contributor. In this case, the CESG cannot exceed $7,200. Otherwise, any excess grants must be repaid.

- Roll over to RRSP – You can defer the tax payable on the income withdrawal by rolling it directly into your RRSP or spousal RRSP, provided you have contribution room. The maximum rollover is $50,000 per contributor.

- Withdraw contributions – Contributions made to the plan can be withdrawn at anytime on a tax-free basis. However, any grants paid on these contributions will be repaid to the government.

- Withdraw earnings and growth – You are entitled to withdraw the earnings and growth on the contributions plus the earnings and growth on the grants (the grants themselves are repaid to the government) if you meet certain conditions.

- Roll over to RDSP – If the beneficiary becomes disabled, as of 2014, there is new legislation that will allow you to move the accumulated income to a qualified Registered Disability Savings Plan for the beneficiary. This can be done on a tax-deferred basis with no 20% penalty.

REGISTERED DISABILITY SAVINGS PLAN

People with disabilities and their loved ones face a distinct set of financial challenges throughout their lives. To help address these challenges, the Government of Canada introduced the Registered Disability Savings Plan (RDSP) in 2008. Designed to help build long-term financial security for disabled persons, the RDSP makes it easier to accumulate funds by providing assisted savings and tax-deferred investment growth.

To qualify to be the beneficiary of an RDSP, an individual must:

- Be eligible for the Disability Tax Credit

- Be a resident of Canada

- Be less than 60 years of age

- Have a valid Social Insurance Number (SIN)

CANADA DISABILITY SAVINGS GRANTS (CDSG)

CDSGs are matching grants that the Government will deposit into the beneficiary’s RDSP to help accumulate savings. The Government provides matching grants of up to 300%, depending on the amount contributed and the family net income.

| FAMILY NET INCOME (2019) | CDSG MATCHING RATES | MAXIMUM ANNUAL CDSG |

| Up to or equal to $93,208 |

300% on first $500 200% on next $1,000 |

$3,500 |

| Over $93,208 | 100% on first $1,000 | $1,000 |

WITHDRAWING YOUR MONEY

RDSP withdrawals must begin by the end of the year you turn age 60. You may withdraw funds earlier, but be sure to note that once a withdrawal of any amount is made, $3 worth of federal grants and bonds paid into the RDSP in the previous 10 years have to be repaid for every $1 withdrawn. Withdrawals will consist of non-taxable contributions, taxable Government monies and taxable growth.

For full information on RDSPs and Government grants and bonds, visit the Government of Canada website.

KEY BENEFITS OF AN RDSP

- Money contributed grows tax free.

- Anyone can contribute to an RDSP with the written consent of the account holder.

- Contributions can be matched, based on family income, with up to $3,500 a year in Canada Disability Savings Grants (CDSG) and up to $1,000 a year in Canada Disability Savings Bonds (CDSB).

- Carry forward on CDSG and CDSB is available back 10 years or to date of diagnosis.

- The total lifetime contribution for each beneficiary is $200,000, with no annual contribution limits.

- If a parent or grandparent passes away and has a financially dependent child or grandchild, they can transfer up to $200,000 of their RRSP/RRIF or RPP to the dependent’s RDSP on a tax-deferred basis.

TAKE ADVANTAGE OF GOVERNMENT HELP

Canada Disability Savings Grant

Through the CDSG, the Government deposits money into your RDSP to help you save, providing matching grants of 300%, 200% or 100%, depending on the amount contributed and the beneficiary’s family net income. The maximum is $3,500 each year, with a lifetime limit of $70,000.

Canada Disability Savings Bond

Through the CDSB, the Government deposits money into the RDSPs of low-income and modest-income Canadians. If you qualify for the bond, you could receive up to $1,000 a year, with a lifetime limit of $20,000.

ETF Portfolios provide:

- Cost effectiveness

- Multi-level diversification

- Risk-based asset allocation

- Transparency

- Access to a broad range of investments

ETF's - EXCHANGE TRADED FUNDS

Since ETFs were first offered, they have evolved to offer a range of benefits and are managed using a variety of different approaches. ETFs remain one of the most popular and innovative investment solutions available to investors.

To help address an investor’s risk profile, mitigate impact of market volatility and deliver an appropriate investment mix, we offer risk-based asset allocation solutions with ETF Portfolios. These multi-asset portfolios are constructed using a combination of Exchange Traded Funds to create a one-ticket solution.

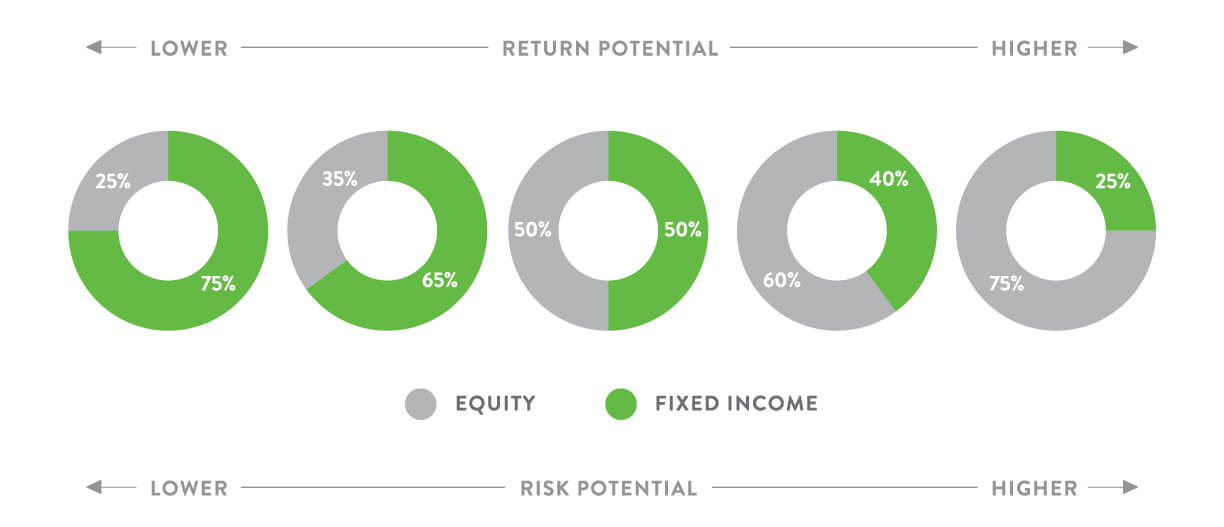

Different target portfolios for different risk appetites

No two investors are alike. That’s why our ETF Portfolios offer five target risk profiles, each uniquely designed to maximize return potential for a given level of risk.

THE VALUE OF FINANCIAL ADVICE

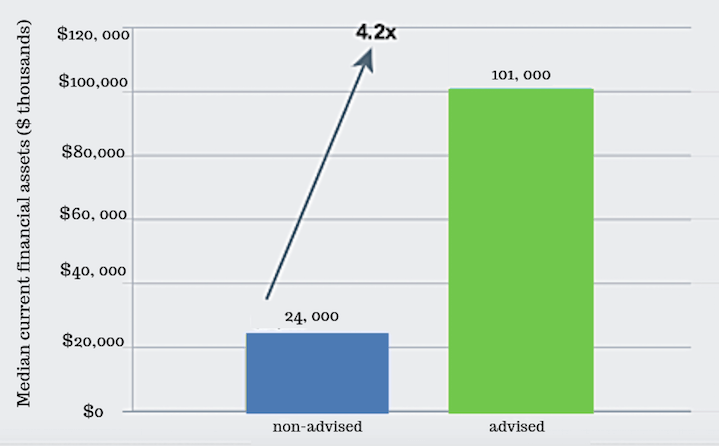

Advised households save at TWICE the rate of Non-Advised households!

Financial advice has a positive and significant impact on accumulating financial assets

The chart displays median asset levels for the Advised and Non-Advised households. As illustrated, the Advised households have 4.2 times the median assets of the Non-Advised households.

*Source: New evidence on the value of financial advice. By Dr. Jon Cockerline, Ph.D.